What is a Credit Score?

A credit score is a numerical representation of your creditworthiness, calculated using a mathematical formula. Scores range from 300 to 850—the higher your score, the more likely you are to be approved for loans with favorable terms. Conversely, a low credit score can make it harder to secure credit and often results in higher interest rates. A high credit score can save you thousands of dollars over the life of a mortgage, auto loan, or credit card.

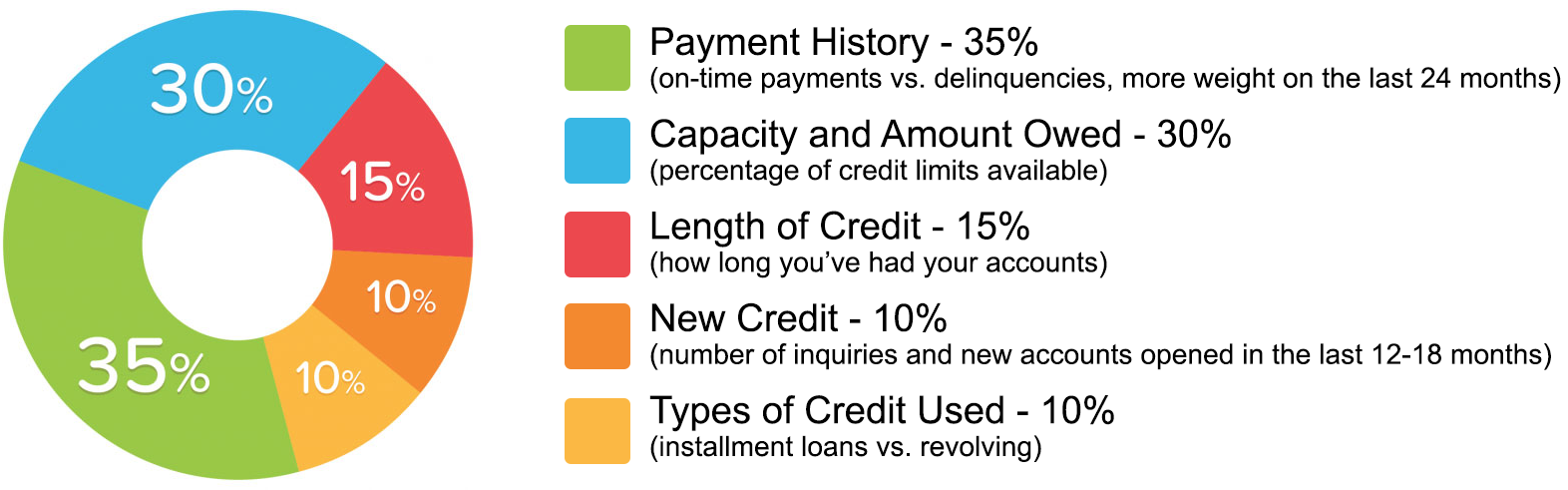

What Affects Your Credit Score?

We offer expert assistance in improving your credit score through:

- Disputing negative items in your payment history.

- Maximizing your debt ratio score—even if paying off credit cards isn't immediately possible.

- Removing credit inquiries from your credit report.

Why Credit Scores Differ Across Bureaus?

The three major credit bureaus--Equifax, Experian, and TransUnion—often report different credit scores due to variations in reported items. On average, the score difference between the highest and lowest bureau is 60 points. This discrepancy can arise from incomplete, incorrect, or non-compliant reporting.

Common Credit Report Issues

A recent study found that nearly 80% of credit reports contain serious errors. Many reports also have minor inaccuracies that we specialize in addressing. If we cannot remove at least 25% of the negative credit items from all three of your credit reports, we will refund 100% of your fee.

Tips for Improving Your Credit Score

- Pay Bills on Time Always pay bills—utilities, mortgage, auto loans, and credit cards—by their due dates.

- Monitor Your Credit Report Check your credit report at least once a year. You can challenge inaccuracies; learn how to do so here.

- Manage Credit Card Balances

- Never charge more than 30% of your available credit limit.

- Reduce balances below 30% for a positive impact on your score.

- Use credit cards strategically—run small recurring charges (like utilities) and pay them off in full each month.

- Keep Credit Accounts Open Even unused accounts can help your score. Use them occasionally for small purchases and pay off balances promptly.

- Be Patient Building or repairing your credit takes time. Consistently following these practices will gradually improve your score and qualify you for better loan terms and interest rates.

How Long Items Remain on Your Credit File?

- Delinquencies (30–180 days): 7 years from the initial missed payment.

- Collection Accounts: 7 years from the original delinquency date, marked as "paid collection" if resolved.

- Charge-Off Accounts: 7 years from the original missed payment, even if later payments are made.

- Closed Accounts:

- With delinquencies: 7 years from closure.

- Positive accounts: 10 years from closure.

- Lost Credit Cards: 2 years if no delinquencies; prior delinquencies reported for 7 years.

- Bankruptcy:

- Chapters 7, 11, and 12: 10 years from filing.

- Chapter 13: 7 years from filing.

- Judgments: 7 years from filing.

- Tax Liens:

- Unpaid: 15 years.

- Paid: 10 years.

- Inquiries:

- Most inquiries: 2 years.

- Employment or pre-approved offers: Visible only on personal credit reports.

Information Excluded from Credit Reports

- Medical information (unless you provide consent).

- Bankruptcies older than 10 years.

- Debts older than 7 years (including delinquent child support).

- Age, marital status, or race (in employment-related credit checks).